April 2, 2026. One year ago today, President Trump announced sweeping reciprocal tariffs on nearly every U.S. trading partner in what the White House dubbed “Liberation Day.” The announcement imposed import duties ranging up to 50%, with a 10% baseline rate on most countries with more tariffs announced recently. The policy landscape has since been turbulent, and the Supreme Court ruled in February 2026 that the IEEPA-based tariffs were unconstitutional, though the administration moved quickly to reimpose duties through other statutory authorities. But for CPG brand teams, the legal back-and-forth is almost beside the point. The cost pressures are real, they are building, and they are arriving at exactly the worst moment for consumer tolerance.

According to analysts at Spins, the tariff fallout for CPGs is expected to land between April and October 2026. Tariff-driven cost increases typically lag 12 to 18 months through the supply chain, and “it is in 2026, and potentially even late 2026, that we will start to see consumers feel a pinch.” Manufacturers and retailers have largely absorbed these costs to date, but that buffer is running out.

The result is a decision that sits on the desk of virtually every CPG brand leader right now: raise prices and risk volume, or absorb the margin hit and risk the business. It’s a false binary and the brands that realize that will be the ones that come out ahead.

The supply chain and pricing research is unambiguous about what’s at stake

The consumer intelligence community has been clear-eyed about what CPG companies are walking into. BCG has called the current environment “brutal” for CPG companies, describing consumer spending that is slowing as households cut back, trade down, and turn to private-label products, while “tariff volatility creates additional uncertainty.”

Deloitte’s 2026 Consumer Products Outlook found that over half of CPG executives surveyed expect they will need to raise prices due to international trade policies. But raising prices into a consumer base that is already stretched is a high-wire act.

NielsenIQ’s Consumer Outlook for 2026 found that 95% of consumers say trust is critical when choosing a brand, and that private label is delivering +3.6% growth globally, with double-digit growth in Western Europe, as shoppers increasingly see it as delivering value without compromise. In that context, a poorly executed price increase isn’t just a volume risk. It’s a brand equity risk to monitor.

NIQ’s data shows that only 12% of consumers are willing to stick to their regular brand regardless of price, a sobering benchmark for anyone assuming that loyalty will insulate their brand from the pricing decision they’re about to make.

McKinsey’s latest CPG analysis notes that “consumer confidence remains uneven, tariffs continue to add pressure, and macroeconomic uncertainty remains” and that consumers in 2026 will likely keep focusing on value because of ongoing price sensitivity, higher living costs, and growing trust in the quality of private-label brands.

The picture is consistent across every major research house: consumers are not in a forgiving mood, and brand loyalty is being renegotiated in real time. As eMarketer observed, consumer-goods makers “can no longer count on inflation-weary shoppers to accept price increases,” yet companies still need to recover higher input costs.

The pricing decision is actually a brand intelligence problem

Here is where most brands get it wrong. They treat the pricing question as a revenue management problem, a spreadsheet exercise involving cost inputs, elasticity models, and competitive price ladders. And it is all of those things. But it’s also a brand problem, because every price change sends a signal to consumers about what your brand stands for and how it values the relationship.

The brands navigating this well are distinguishing between products in their portfolio that can weather price rises and those that cannot. Premium or differentiated goods are most ripe for increases, especially among brand-loyal consumers, while middle-tier products that can be replaced by alternatives require more caution given consumer willingness to trade down.

That distinction of which products can absorb a price increase and which ones will bleed volume is not made at the spreadsheet level. It’s made at the brand equity level informed by brand equity AI platforms like Brand Pulse and SKU-level product CX listening like CX Bench. Specifically, it’s made by understanding your price/value equation with precision at the brand, segment and SKU level.

At i-Genie.ai, we call this dimension “Value”, and it’s one of the core components of Brand Score in Brand Pulse, our continuous brand equity intelligence platform. Value captures how consumers perceive the relationship between what they pay and what they get. It’s not just a sentiment score. It’s a diagnostic that tells you where your pricing power actually lives and where it doesn’t. As Stan says, “premium is not a price point!“

Here’s how Brand Pulse changes the decision.

Three scenarios where Brand Pulse’s Value Dimension changes everything

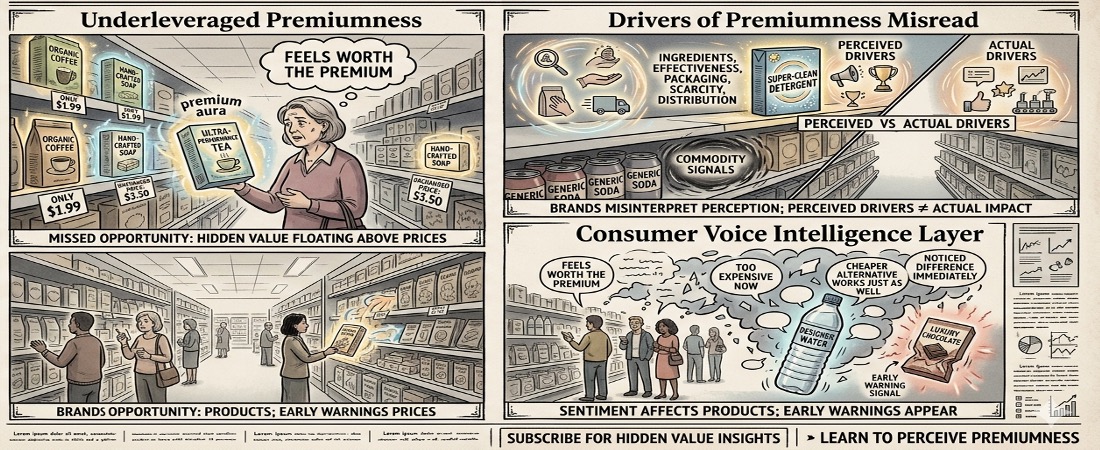

Scenario 1: You have a high Value score and you don’t know what to do with it

Some brands carry genuine pricing permission that they’ve never fully leveraged. A high Value score in Brand Pulse means consumers consistently perceive your brand as worth more than what they’re paying: that the value they receive exceeds the price they pay. That is, in the current moment, an extraordinary asset.

The mistake brands make is treating a high Value score as evidence that everything is fine, rather than as a strategic resource. If your consumers believe you are underpriced relative to your value, a measured price increase is not just defensible, it may actually reinforce the premium perception! Brands that command premium positioning and then hold prices when costs rise can inadvertently signal that they were never premium to begin with.

Brand Pulse allows teams to monitor Value in real time so that when a price change goes into effect, they can immediately track whether that premium perception holds, strengthens, or begins to erode and respond with messaging, trade support, or promotional strategy before any brand damage compounds.

Scenario 2: You know your Value score, but you don’t know what’s driving it

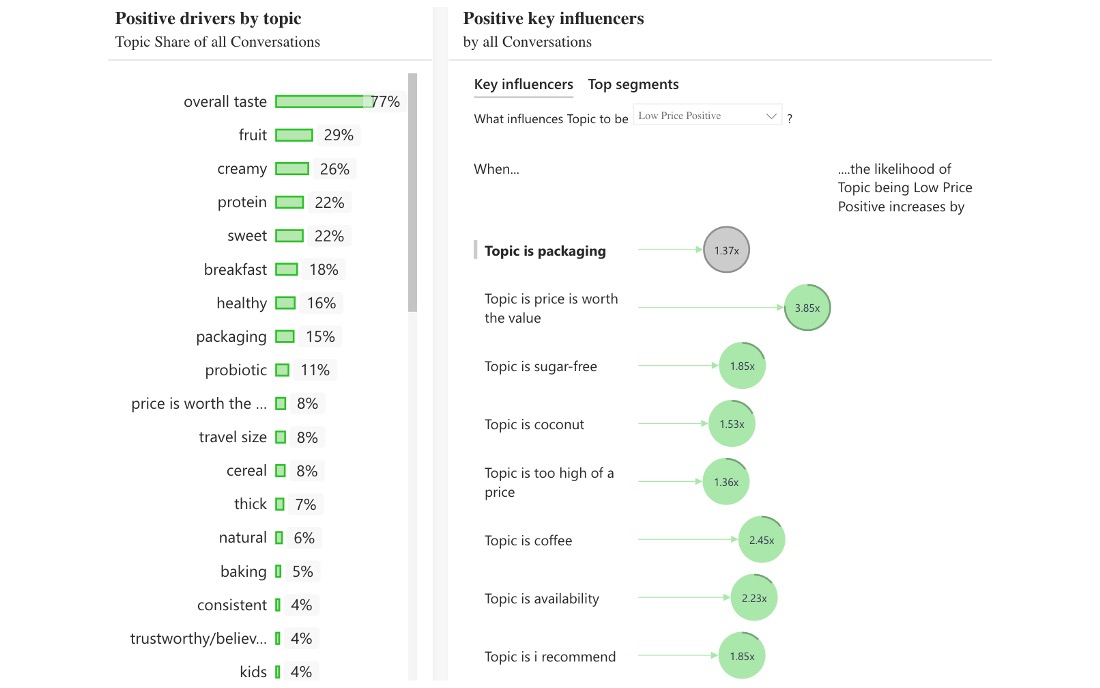

An aggregate Value score is a starting point. The more powerful capability is understanding the positive and negative drivers underneath it, especially the specific attributes that are making consumers feel the price is worth it, and the friction points that are undermining that perception.

Brand Pulse‘s driver analysis breaks Value into its components. For a personal care brand, positive drivers might be concentrated around ingredient quality and efficacy claims, while a negative driver might be packaging that reads as commodity rather than premium. For a food brand, Value might be carried almost entirely by taste and heritage, but undermined by a perception that the brand is widely available at discount retail, which erodes the scarcity and exclusivity signals.

Brand Pulse shows the positive and negative drivers of Price/Value perception so you can understand what SKUs, segments, ingredients or benefits are stronger and which marketing messages reinforce value.

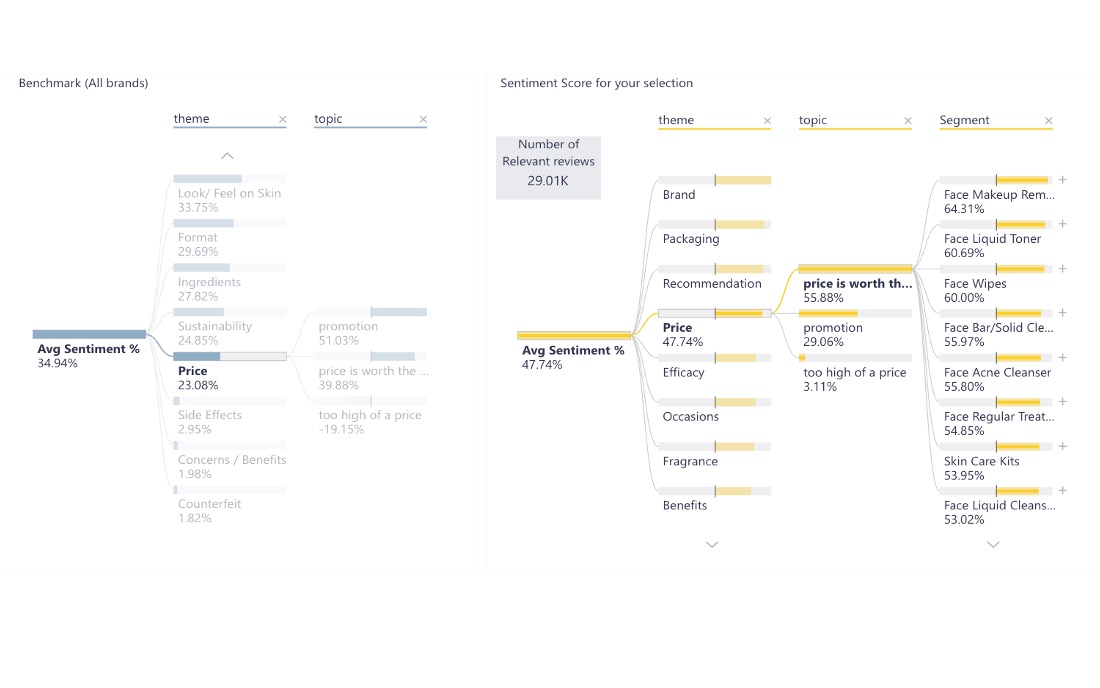

And with CX Bench, you can drive to the Segment, Sub-Segment or SKU level to understand the sentiment and topics of “price,” so you can respond with highly targeted marketing campaigns or Product Detail Page (PDP) optimization. Here you can see a brand that has much higher net sentiment in price, and exactly what segments have the highest sentiment of “price is worth the value.”

CX Bench shows specific sentiment analyses from reviews, showing which SKUs and segments have positive and negative net sentiment.

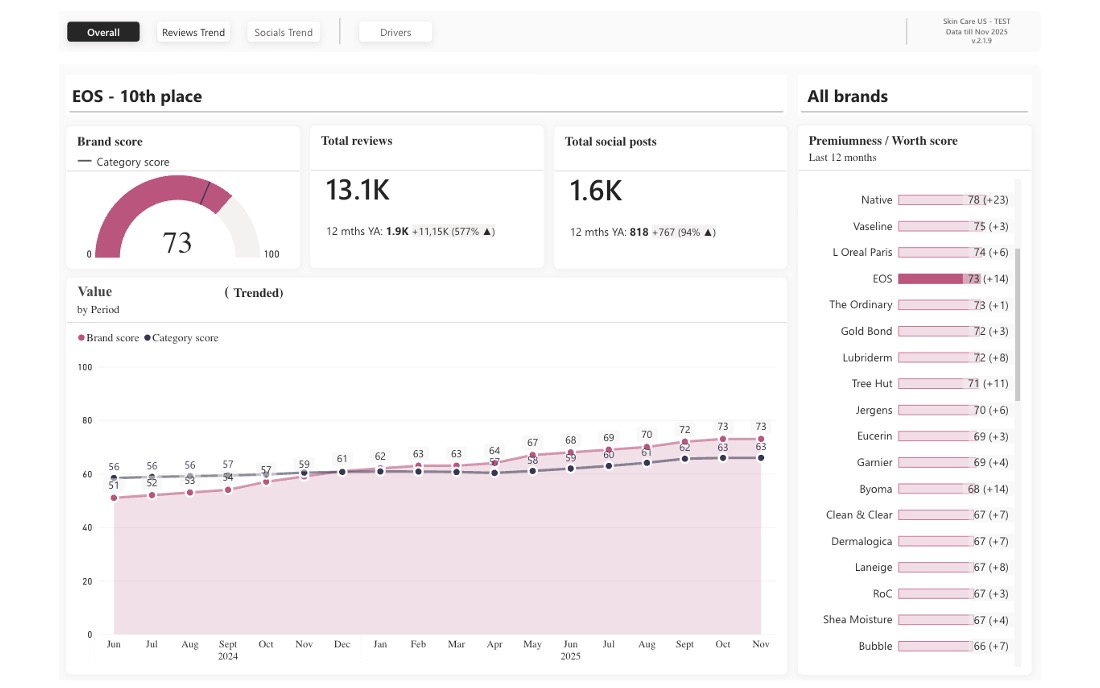

Value can be trended over time and ranked by competitors. Here EOS is well poised for absorbing a price increase, having gone from below category average to above category average.

Value can be trended over time and ranked by competitors. Here EOS is well poised for absorbing a price increase, having gone from below category average to above category average.

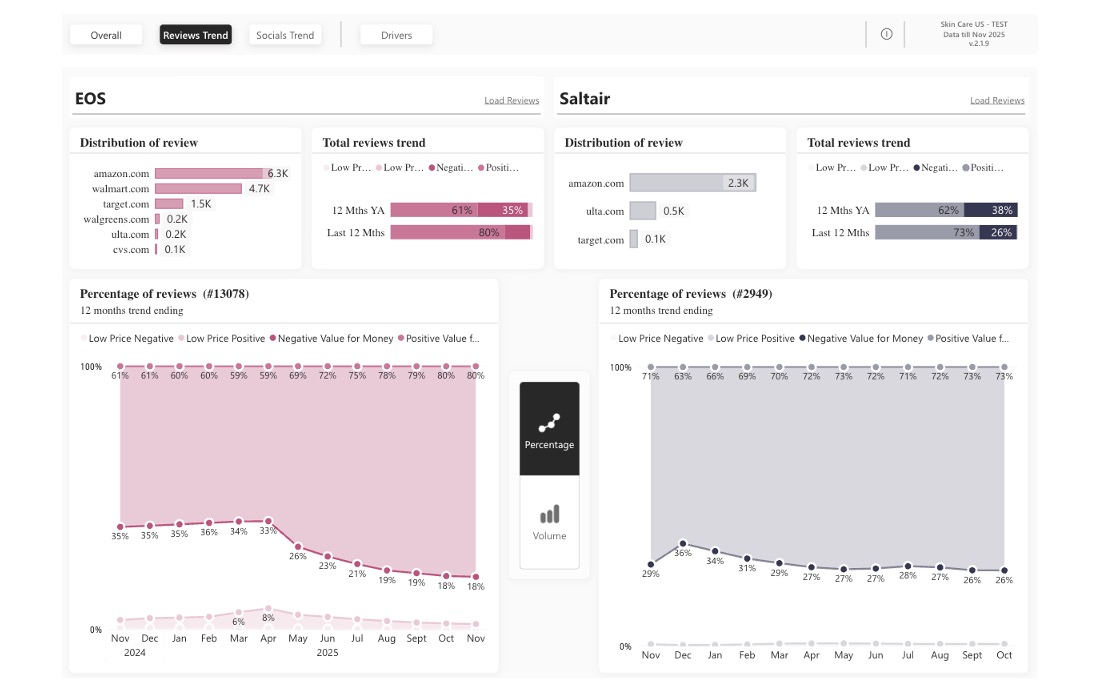

And you can diagnose where sentiment is coming from at the channel and retailer level and do a head-to-head comparison against key competitors, including projecting how their pricing strategy might lead to market share opportunities. Here EOS is seeing significant positive trends in “Positive Value For Money” especially in contrast to competitor Saltair.

This matters enormously for pricing decisions. If your Value is driven by efficacy, you can raise prices and lean into benefit communication to reinforce the value. If it’s undermined by distribution channel perception, a price increase without a channel strategy could accelerate volume loss. Knowing the drivers doesn’t just tell you whether to raise prices, it tells you what to do alongside the price change to protect and extend your equity.

Scenario 3: You have driver data, but you need to know what consumers are saying

Driver data tells you what is influencing Value. Verbatim consumer language tells you how, and that how is what gives brand and marketing teams the precision to act. i-Genie.ai is decision-grade data with actionability.

Brand Pulse ingests consumer language from social media, reviews, forums, and digital channels, and maps it directly to Brand Score dimensions including Value. This means a brand team can see not just that “efficacy” is a positive driver of their premium perception, but the specific language consumers use to describe it: “lasts all day without reapplication,” “works better than anything I’ve paid twice as much for,” “I noticed a difference in the first week.” That’s the language that belongs in your price-increase communication strategy.

Equally important is the negative verbatim. If consumers are saying things like “great product but starting to feel expensive for what it is,” or “I used to think this was worth the premium but I’ve found a cheaper alternative that works just as well,” that is the early warning signal that your pricing headroom is narrowing. Caught in a quarterly tracker, that signal arrives too late to act on. Caught in Brand Pulse, it arrives in time to course-correct.

This is the capability that separates brands that make pricing decisions from brands that make informed pricing decisions with action plans to reinforce marketing and mitigate risk.

This critical pricing moment calls for a new kind of brand monitoring

The coming price shock for CPG brands is not hypothetical. Analysts warn that avoidance of sharp price hikes so far “reflects timing, not immunity” and that the impact will likely follow the same cost-shock playbook as commodity price increases, with the added variable of political uncertainty.

NielsenIQ’s brand equity analysis for 2026 is direct: “The most successful brands won’t be the loudest; they’ll be the easiest for consumers to choose and the hardest for them to replace.” That outcome requires understanding what makes your brand irresistible, and fixing the specific levers that drive strength.

Price is one of those levers. Managed well, it reinforces your brand’s premium story. Managed poorly, it unravels equity that took years to build.

The question is not whether to raise prices. For many brands, that decision has already been made by the cost environment. The question is: do you have the brand intelligence infrastructure to make that decision surgically, knowing which products can take it, understanding what’s driving your Value perception, and hearing directly from consumers what they’re saying about your price/value equation right now?

")